Car insurance comprehensive vs collision – two terms often thrown around but not always fully understood. Both are essential components of a robust car insurance policy, but they protect against very different types of events. This article dives into the specifics of each coverage, exploring their differences, benefits, and how to choose the right level of protection for your needs.

Navigating the world of car insurance can feel overwhelming, especially when faced with terms like comprehensive and collision. Understanding these coverages is crucial, as they can significantly impact your financial well-being in the event of an unexpected incident. We’ll break down the intricacies of each, highlighting their key features, and providing valuable insights to help you make informed decisions about your car insurance.

Car Insurance: Comprehensive vs. Collision: Car Insurance Comprehensive Vs Collision

Car insurance is essential for protecting yourself financially in the event of an accident or other damage to your vehicle. It provides a safety net, helping you cover repair costs, medical expenses, and other related liabilities. Two key types of coverage are comprehensive and collision, and understanding their differences is crucial for making informed decisions about your insurance policy.

Comprehensive and Collision Coverage Explained

Comprehensive and collision coverage are two distinct types of car insurance that protect you from different types of risks. They work together to provide comprehensive protection for your vehicle. Here’s a breakdown of each:

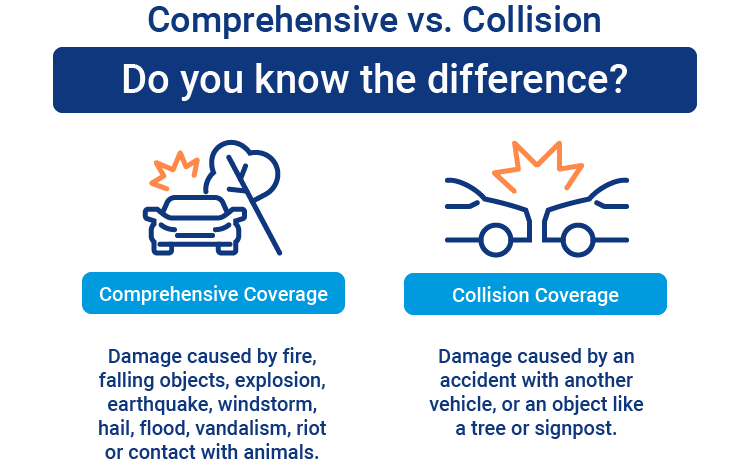

- Comprehensive Coverage: This coverage protects your vehicle against damage caused by events other than collisions, such as theft, vandalism, fire, natural disasters, and falling objects. It also covers damage caused by animals, such as a deer colliding with your car.

- Collision Coverage: This coverage protects your vehicle against damage caused by a collision with another vehicle or an object, such as a tree or a pole. This includes accidents where you are at fault, as well as those where you are not at fault.

Comprehensive Coverage

Comprehensive coverage is a type of car insurance that protects you against damage to your vehicle from events other than collisions. It essentially covers your car against risks that are outside of your control.

Covered Events

Comprehensive coverage protects you from a wide range of events, including:

- Theft: If your car is stolen, comprehensive coverage will pay for the cost of replacing or repairing it, minus your deductible. This includes cases of carjacking, where the car is taken by force, and situations where the car is stolen while parked in a public place or at home.

- Vandalism: If your car is damaged by vandalism, comprehensive coverage will pay for the repairs, minus your deductible. Vandalism can include acts like keying the paint, breaking windows, or spray painting the car.

- Natural Disasters: Comprehensive coverage can protect your car from damage caused by natural disasters, such as hurricanes, tornadoes, floods, earthquakes, and hailstorms. For example, if your car is damaged by a hailstorm, comprehensive coverage will pay for the repair or replacement of the damaged parts.

- Fire: If your car is damaged by fire, comprehensive coverage will pay for the repairs, minus your deductible. This includes situations where the fire is caused by a mechanical malfunction, an electrical short, or an external source.

- Falling Objects: Comprehensive coverage can also cover damage caused by falling objects, such as tree branches, rocks, or hail. If a tree branch falls on your car, comprehensive coverage will pay for the repairs or replacement of the damaged parts.

- Animal Collisions: If your car is damaged by a collision with an animal, comprehensive coverage will pay for the repairs, minus your deductible. This includes situations where the animal is a deer, a bird, or a dog.

Factors Affecting Premiums

Several factors can influence the cost of your comprehensive coverage premiums, including:

- Vehicle Value: The higher the value of your car, the more expensive your comprehensive coverage will be. This is because the insurance company will have to pay more to replace or repair your car if it’s damaged.

- Vehicle Age: Older cars generally have lower comprehensive coverage premiums than newer cars. This is because older cars are less expensive to replace or repair. However, if your car is very old, it may be difficult to find comprehensive coverage.

- Driving History: If you have a history of accidents or traffic violations, your comprehensive coverage premiums will be higher. This is because you are considered a higher risk to the insurance company.

- Location: Comprehensive coverage premiums can vary depending on your location. For example, if you live in an area with a high rate of theft or vandalism, your premiums will be higher.

- Deductible: Your deductible is the amount of money you pay out-of-pocket before your insurance coverage kicks in. The higher your deductible, the lower your comprehensive coverage premiums will be. However, you will have to pay more out-of-pocket if you make a claim.

Collision Coverage

Collision coverage protects your vehicle from damage caused by a collision with another vehicle or object. It covers the cost of repairs or replacement, minus your deductible.

Covered Events

Collision coverage protects your vehicle from damage caused by a collision with another vehicle or object. Here are some examples of events covered by collision coverage:

- An accident with another vehicle

- Hitting a stationary object, such as a tree, pole, or fence

- Rolling your vehicle over

- Being hit by an uninsured or underinsured motorist

Factors That Determine Collision Coverage Premiums

Several factors influence the cost of collision coverage. These include:

- Your vehicle’s make, model, and year: Newer and more expensive vehicles are generally more costly to repair or replace, resulting in higher premiums.

- Your driving history: Drivers with a history of accidents or traffic violations are considered higher risks and will typically pay more for collision coverage.

- Your location: Collision coverage premiums can vary depending on your location. For example, areas with high traffic density or a higher rate of accidents may have higher premiums.

- Your deductible: The deductible is the amount you pay out of pocket before your insurance company covers the rest of the repair costs. A higher deductible generally means lower premiums. However, you will need to pay more out of pocket if you have to file a claim.

- Your insurance company: Different insurance companies have different pricing structures. It’s essential to compare quotes from multiple companies to find the best rates.

Key Differences

Comprehensive and collision insurance are two essential types of car insurance coverage, offering protection against different risks. While both protect your vehicle, they cover distinct events, making it crucial to understand their differences to ensure adequate coverage.

Coverage Provided

The main difference between comprehensive and collision coverage lies in the types of events they cover. Comprehensive insurance protects your vehicle against damages caused by non-collision events, while collision coverage protects against damages caused by accidents involving another vehicle or object.

Types of Events Covered

Understanding the specific events covered by each type of insurance is crucial to determining the right coverage for your needs.

- Comprehensive Coverage covers damages caused by events such as:

- Theft

- Vandalism

- Fire

- Hail

- Flooding

- Windstorms

- Animal collisions

- Acts of nature

- Collision Coverage covers damages caused by events such as:

- Accidents involving another vehicle

- Accidents involving an object, such as a tree or pole

- Rollover accidents

- Single-vehicle accidents

Situations Where Each Coverage is Essential

The need for each type of coverage depends on various factors, including the value of your vehicle, your driving habits, and the risk of exposure to certain events.

- Comprehensive Coverage is essential in situations where:

- Your vehicle is parked in a high-crime area, increasing the risk of theft or vandalism.

- You live in an area prone to natural disasters such as hailstorms, floods, or wildfires.

- Your vehicle is a luxury or high-value car.

- Collision Coverage is essential in situations where:

- You drive frequently in congested areas with a high risk of accidents.

- You are a new or inexperienced driver, increasing the risk of accidents.

- Your vehicle is financed or leased, as the lender or leasing company typically requires collision coverage.

Deductibles

A deductible is the amount of money you agree to pay out of pocket before your insurance coverage kicks in. It’s a way to lower your insurance premiums, but it means you’ll have to pay a portion of the repair or replacement costs yourself.

Deductibles apply to both comprehensive and collision coverage, but they’re separate for each type of coverage. This means you might have a $500 deductible for comprehensive coverage and a $1,000 deductible for collision coverage.

How Deductibles Affect Insurance Payouts

Deductibles influence the amount your insurance company will pay for covered repairs or replacements. Here’s how it works:

Let’s say your car is damaged in an accident and you have collision coverage with a $500 deductible. The total cost of repairs is $2,000. You’ll pay the first $500 (your deductible), and your insurance company will cover the remaining $1,500.

Examples of Deductibles in Real-World Scenarios, Car insurance comprehensive vs collision

- Comprehensive Coverage: Your car is stolen, or damaged by a falling tree. You have a $250 deductible. The insurance company will cover the remaining cost of replacing or repairing your car, minus your deductible.

- Collision Coverage: You’re in an accident and damage your car. You have a $1,000 deductible. Your insurance company will cover the remaining cost of repairs, minus your deductible.

Factors Influencing Coverage

Several factors play a significant role in determining the cost of comprehensive and collision coverage. These factors are assessed by insurance companies to evaluate your risk and calculate your premiums.

Vehicle Type

The type of vehicle you drive is a major factor influencing insurance premiums. This is because different vehicles have varying repair costs, theft risks, and safety ratings.

- Luxury or high-performance vehicles are often more expensive to repair and are more likely to be targeted for theft, leading to higher premiums.

- Older vehicles, while typically cheaper to purchase, may have higher repair costs due to the availability of parts and the complexity of repairs.

- Vehicles with safety features like anti-theft systems, airbags, and anti-lock brakes often receive lower premiums due to their reduced risk of accidents and injuries.

Driving History

Your driving history is another key factor influencing insurance premiums. This includes your driving record, which reflects your past driving behavior and accident history.

- A clean driving record with no accidents or violations will typically result in lower premiums.

- Accidents or violations on your record can significantly increase your premiums, as they indicate a higher risk of future accidents.

- Traffic tickets, even minor ones, can increase your premiums, as they suggest a higher risk of future accidents.

Location

Your location plays a role in insurance premiums due to the varying levels of risk associated with different areas.

Understanding the difference between comprehensive and collision car insurance is crucial for protecting your vehicle. Comprehensive coverage protects against damage caused by events like theft or natural disasters, while collision coverage covers damage resulting from an accident. For those who also own a motorcycle, you might want to consider car bike insurance to ensure both your vehicles are adequately covered.

Returning to car insurance, it’s important to evaluate your individual needs and driving habits to determine the best coverage for your situation.

- Areas with higher crime rates may have higher premiums for comprehensive coverage due to increased risk of theft and vandalism.

- Areas with heavy traffic may have higher premiums for collision coverage due to increased risk of accidents.

- Areas with severe weather conditions may have higher premiums for both comprehensive and collision coverage due to increased risk of damage from natural disasters.

Other Factors

Other factors can also influence your insurance premiums, including:

- Age and gender: Younger drivers and male drivers often face higher premiums due to their statistically higher risk of accidents.

- Credit score: In some states, insurance companies use credit score as a factor in determining premiums. Individuals with good credit scores may receive lower premiums.

- Marital status: Married individuals often receive lower premiums than single individuals, as they are statistically less likely to be involved in accidents.

- Vehicle usage: The frequency and purpose of vehicle usage can influence premiums. Individuals who drive their vehicles frequently or for long distances may have higher premiums.

- Deductible amount: Choosing a higher deductible can lower your premium, as you are taking on more financial responsibility in the event of an accident.

Choosing the Right Coverage

Determining the appropriate level of comprehensive and collision coverage requires careful consideration of your individual needs and financial situation. You must weigh the potential benefits of having this coverage against the cost of premiums. Several factors influence the decision, and it’s essential to understand them to make an informed choice.

Factors to Consider

Understanding the factors influencing the decision-making process is crucial for choosing the right coverage. These factors provide a framework for evaluating your needs and making an informed decision.

- Your Vehicle’s Value: The value of your vehicle is a significant factor. If your car is relatively new or has a high market value, comprehensive and collision coverage might be more worthwhile. The insurance payout in case of an accident or damage could help you replace or repair your vehicle. On the other hand, if your vehicle is older or has a lower market value, the cost of comprehensive and collision coverage might not be justifiable, especially if you can afford to replace it out of pocket.

- Your Financial Situation: Your financial situation plays a critical role in determining the level of coverage you need. If you can afford to pay for repairs or replacement costs out of pocket in case of an accident or damage, you might consider opting for lower coverage limits or even forgoing comprehensive and collision coverage altogether. However, if you can’t afford to cover such costs, having comprehensive and collision coverage can provide financial security and peace of mind.

- Your Driving Habits: Your driving habits also influence the decision. If you frequently drive in areas with high traffic density or adverse weather conditions, the risk of accidents and damage to your vehicle increases. In such cases, having comprehensive and collision coverage can be more beneficial. Conversely, if you drive less frequently or in areas with lower risk, you might consider opting for lower coverage limits or even forgoing comprehensive and collision coverage.

- Your Personal Risk Tolerance: Your personal risk tolerance is another crucial factor. Some individuals are more comfortable taking risks and might be willing to accept the potential financial burden of an accident or damage without coverage. Others might prefer the peace of mind that comprehensive and collision coverage provides, even if it comes at a higher cost.

Finding the Best Insurance Policy

Finding the best insurance policy at an affordable price requires careful research and comparison. It’s essential to consider various factors and utilize available resources to make an informed decision.

- Compare Quotes from Multiple Insurers: Obtaining quotes from multiple insurance companies is crucial to ensure you’re getting the best possible price for the coverage you need. You can use online comparison websites or contact insurers directly to get quotes.

- Consider Discounts: Many insurance companies offer discounts for various factors, such as safe driving records, good credit scores, multiple policy discounts, and safety features in your vehicle. Inquire about available discounts to potentially lower your premium.

- Review Your Policy Regularly: It’s essential to review your insurance policy regularly to ensure it still meets your needs and that you’re not paying for coverage you don’t need. You might need to adjust your coverage levels as your circumstances change, such as buying a new vehicle or changing your driving habits.

- Understand Your Deductible: Your deductible is the amount you pay out of pocket before your insurance coverage kicks in. A higher deductible generally results in lower premiums, while a lower deductible leads to higher premiums. Consider your financial situation and risk tolerance when choosing your deductible.

Additional Considerations

While comprehensive and collision coverage are essential, there are other crucial aspects of car insurance that you should consider. These additional considerations can significantly impact your financial protection in the event of an accident or other unforeseen events.

Uninsured/Underinsured Motorist Coverage

This coverage protects you if you’re involved in an accident with a driver who is uninsured or whose insurance coverage is insufficient to cover your losses. It’s vital because it provides financial protection for your medical expenses, lost wages, and property damage.

For example, if you’re hit by an uninsured driver who causes significant damage to your car and injuries to you, uninsured/underinsured motorist coverage will help cover your costs, even if the at-fault driver doesn’t have insurance.

Rental Car Coverage

This coverage helps cover the cost of a rental car if your vehicle is damaged or stolen and is being repaired. This coverage can be a lifesaver if you rely on your car for daily commutes, work, or errands.

For example, if your car is totaled in an accident, rental car coverage will help you rent a car while your insurance company handles the claim and you wait for your new vehicle.

Other Relevant Factors

- Roadside Assistance: This coverage provides assistance for situations like flat tires, dead batteries, and lockouts. It’s a valuable addition for peace of mind, especially if you often drive long distances or in remote areas.

- Gap Insurance: This coverage helps pay the difference between your car’s actual cash value and the amount you owe on your car loan if your vehicle is totaled. It’s particularly beneficial if you have a new car or a loan with a longer term.

- Custom Coverage: If you have a car with modifications or unique features, you may need additional coverage to ensure adequate protection. This coverage can help protect your investment in these upgrades.

Conclusion

This article has provided a comprehensive overview of comprehensive and collision coverage in car insurance. By understanding the differences between these coverages, you can make informed decisions about the protection you need for your vehicle.

Key Takeaways

- Comprehensive coverage protects your vehicle against damage caused by non-collision events, such as theft, vandalism, fire, and natural disasters.

- Collision coverage protects your vehicle against damage resulting from accidents, regardless of who is at fault.

- Deductibles are the out-of-pocket expenses you pay before your insurance coverage kicks in.

- Factors such as your vehicle’s value, your driving history, and your location can influence your insurance premiums.

- Choosing the right coverage depends on your individual needs and financial situation.

- Consider factors such as your vehicle’s age, value, and your personal risk tolerance when deciding on coverage.

Importance of Understanding Coverage

It is crucial to understand comprehensive and collision coverage to ensure you have the right protection for your vehicle. Without this knowledge, you could be financially vulnerable in the event of an accident or other incident.

Consult with an Insurance Agent

Ultimately, the best way to determine the right coverage for your needs is to consult with an insurance agent. They can provide personalized advice based on your specific circumstances and help you make informed decisions about your car insurance.

Final Review

Ultimately, choosing the right car insurance coverage is a personal decision. Consider your driving habits, the value of your vehicle, and your risk tolerance. By understanding the nuances of comprehensive and collision coverage, you can tailor your insurance policy to best protect your financial interests and ensure peace of mind on the road. Remember, consulting with an insurance agent can provide personalized guidance and help you find the best coverage at an affordable price.